A deluge of big tech reports, GDP and Jobless claims have come together to create the perfect storm of uncertainty. Today could be very challenging, but the Friday open has the potential to be very wild, and no one knows if the bulls or the bears will leading the charge. Anything is possible, so consider the risk carefully you carry into today’s close. Can they produce earnings strong enough to support current prices? We will find out after the bell today.

Asian markets closed modestly bearish across the board overnight in reaction to the FOMC rate decision. European markets trade cautiously this morning, leaning slightly into the red. US Futures are decidedly bearish this morning, pointing to a gap down open ahead of earnings, GDP and jobless claims. Buckle up the next 24 hours have the potential to be very volatile.

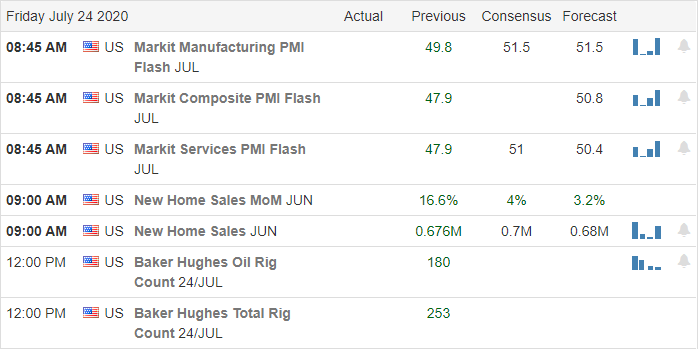

Economic Calendar

Earnings Calendar

All eyes will be on the big tech earnings reports after the bell today. Overall we have more than 250 companies reporting their quarterly results will make it our busiest day so far this season. Notable reports include FB, AMZN, AAPL, GOOGL, AMT, BUD, MT, AZN, TEAM, BAX, CARS, CC, CI, CLF, CMCSA, COF, COR, CS, CROX, DECK, DNKN, ELAN, EA, LLY, EXPE, F, FTS, GPC, GILD, GRUB, HBI, HST, K, KHC, LIN, LTC, MA, MGM, TAP, MCO, NEM, NOC, PG, PFPT, RDFN, SHAK, SIRI, SO, SWK, SYK, SYK, TW, UPS, X, VLO, VRTX, WM, WWE, XLNX, & YUM.

News & Technical’s

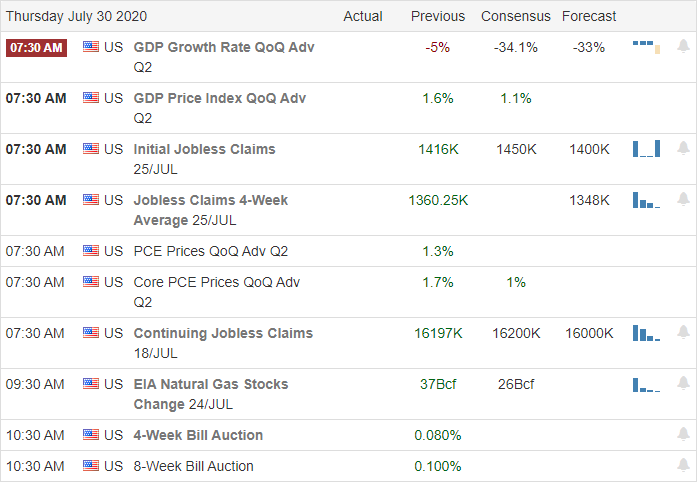

This morning we will likely get an historic reading on the GDP with numbers near the World War 2 economic impacts. The question to be answered is the number already baked into the market’s pricing, or will there be a strong reaction. At the same time will get the latest details on Jobless claims that could begin to creep back up due to the second wave virus impacts. The FOMC yesterday decided to stand fast on interest rates and said the direction of the economy will be tied directly to the length and duration of the pandemic. There are likely to be a lot of fireworks after the bell today as FB, AMZN, APPLE, and GOOGL report quarterly results. The uncertainty surrounding these reports has the market on edge, and traders should expect a wild open on Friday as a result. As Congress haggles over the details of the next stimulus bill, the still found time to hold a virtual flogging of the top tech business accusing them of everything from anticompetitive practices to outright stealing. I’m sure there is much more to come on this subject in the near future.

Even with the uncertainty and very choppy price action, the bulls have maintained majority control over the indexes. However, with such a big day of data coming our way, anything is possible. Going into the close today, traders will have to consider carefully the risk and price volatility we could experience Friday at the open. The potential for a huge gap is high, and the big question yet to be answered is, will it be controlled by the bull or the bear? Your guess is as good as mine.

Markets gapped up about three-tenths of a percent and proceeded to put in a slow, steady all-day rally. As expected, the Fed decision and statement gave no surprises and only the big Tech anti-trust hearings caused any blip at all. However, stocks still closed near their highs. Yet even with a nice candle on the day, no major ground has been gained by the bulls or bears for the week as a whole. The SPY closed up 1.20%, the DIA up 0.59%, and the QQQ up 1.15% for the day. The VXX fell to 28.52 and T2122 climbed well back into the overbought territory at 91.57. 10-year bond yields fell slightly to 0.577% and Oil (WTI) rose slightly to $41.30/barrel.

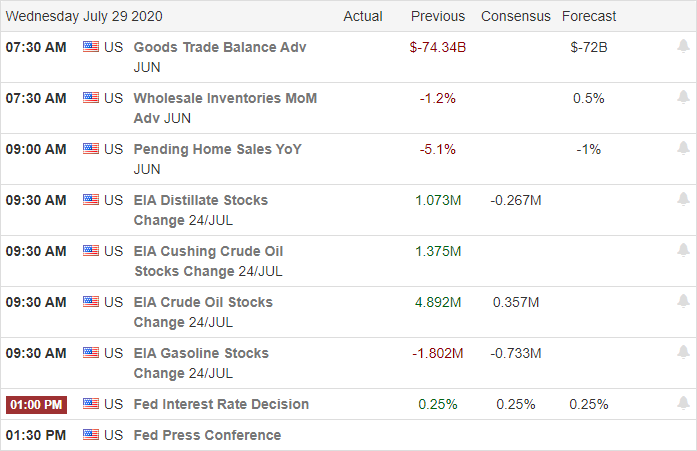

The key takeaway from Fed Chair Powell’s press conference was that the FOMC is “not even thinking about raising rates” and while recovering, “the economy remains well below the levels at the beginning of the year.” So monetary policy should remain full speed ahead on the printing presses. On the Fiscal side, the Democrats and Republicans remain far apart (as well as the Republicans within their own ranks) on another Stimulus bill agreement.

On the Anti-trust hearings, the CEOs of AAPL, AMZN, FB, and GOOG were beaten up with evidence of anti-competitive activities. The CEO’s general approach seemed to be denial or reframing of the allegations. However, Jeff Bezos went a different route, claiming to be shocked and concerned at the accusations. It is worth noting that FB, AMZN, GOOG, and AAPL stocks all rose well over a percent on the day. So, Mr. Market did not care about at least the first couple hours of the process.

In the US, the virus numbers show we have 4,568,375 confirmed cases and 153,848 deaths. With new cases came in at 66,921 Wednesday and deaths rose again to 1,485. TX passed NY to join CA and FL with the distinction of being the most-infected states. This came as another group of scientists called for a second national shutdown. The first group was 150 scientists who wrote an open letter last weekend. Johns Hopkins University Infectious Disease Department scientists became the second group, recommending 10 steps which included a national lockdown and nationally mandatory masks to stem the tide.

Globally, the number of cases has reached 17,213,663 confirmed cases and 670,909 deaths. In Asia, Australia, Hong Kong, India, and Vietnam all had record numbers of new cases while Japan and South Korea were near record highs. In Europe, Italy extended its state of emergency through Oct. 15. This comes as Germany reports the sharpest quarterly economic drop on record (a 10.1% contraction).

Overnight, Asian markets were mixed yet again, but this time lean toward the red. However, the moves were modest. The lone outlier is Taiwan, which was up 1.45%. In Europe, markets are strongly red across the board on poor economic data and a resurgence of cases in a number of EU countries. As of this point, the FTSE is down 1.92%, the DAX down 2.85%, and the CAC down 1.68%. In the US, as of 7:30 am futures are pointing to a once percent gap down across the 3 major indices. However, the economic data at 8:30 am is likely to have a significant impact one way or the other.

The major economic news for Thursday is limited to Q2 GDP and Initial Jobless Claims (both at 8:30 am). Major earnings include AOS, AGCO, ALXN, AMT, BUD, APTV, ARW, AZN, BAX, CARR, CI, CLF, CNHI, CMCSA, COP, DAN, DBD, DD, FNMA, FMCC, FMS, GPC, GPI, HBI, HUBB, IDA, ICE, IP, K, KDP, KHC, LIN, LKQ, LLY, MA, MAS, MCO, MD, MMC, MT, NEM, NOC, ODFL, OSK, PG, SAH, SIRI, SNDR, SO, SWK, TAP, TMHC, TXT, UPS, VLO, WM, WLTW, XEL, XYL, and YUM all before the open. Then AAPL, AJG, AMZN, ATUS, BLDR, CC, DVA, EA, F, FB, FLEX, FLS, GILD, GOOG, HIG, INT, LPLA, MHK, MOH, MTZ, RLGY, SEM, X, VRTX, and XPO all report after the close.

Wednesday gave us a nice candle in an otherwise consolidating last week. With no sign of a stimulus deal yet, it will surely be GDP and Jobless Claims that call the tune for the day. However, there are a lot of important earnings today(but most of the mega-cap tech names are after the close). So, volatility is likely to continue after the news.

Did you ever think you’d see a day when if we were lucky enough to see a 30% GDP contraction, that might be seen as a major beat of estimates? The point is we are in uncharted waters. We really don’t know how good or bad any number will be seen by the overall market. All we know for sure is that bulls have been wearing their rose-colored glasses for some time and that whipsaws are fast.

Keep the FAANG stocks in your line of sight as they will point the way. Follow the trend, don’t try to predict reversals or chase moves that got away. And always, always take profits as you go. Remember, trading is a job and we’re here to consistently make profits, not win the lottery.

Ed

The Daily Swing Trade Ideas for today: OIH, V, SIG, SYF, FITB, FAST, COF. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

There seems to be considerable uncertainty amongst traders and investors facing a big day of earnings and a pending FOMC decision. Yesterday was undoubtedly a frustrating day of intraday whipsaws and choppy price action that culminated in a bearish push reversing the bullish action seen on Monday. What comes next is anyone’s guess, so stay focused and flexible. Remember, there is no shame in standing aside, protecting your capital if you have no edge in such a new driven environment. Cash is a position!

Asian markets closed the day mixed and relatively flat as they wait for the FOMC decision. European markets also trade mixed chopping around the flat-line uncertain about what comes next. US Futures trade flat this morning ahead of a massive day of data with an equal chance of encouraging the bulls or bringing on a bearish attack. Buckle up for the wild ride the next couple days could provide.

The market will have no shortage of data to digest today with 3rd quarter earnings ramping up and including some of the tech giants reporting after the bell. We will also get the FOMC decision at 2 PM Eastern, followed by Jerome Powell’s press conference 30 minutes later. Republicans and Democrats seem to be digging into entrenched position over the next stimulus bill as the two sides step up the rhetoric as they battle between price tags of 1 to 3 trillion of additional deficit spending. Meanwhile, on the coronavirus front, the official death toll from the pandemic crossed 150,000, with more than 65,000 new infections report yesterday. With all this going on, Congress still has the time to bring in several of the top tech company CEO’s to grill them in public hearings.

After a very choppy day of trading, the bears stepped up their activity as we headed into the close yesterday, reversing the bullish action on Monday. Clearly, there remains considerable uncertainty among traders and investors amidst the mixed bag of earnings reports as companies report the impacts of the pandemic. With a slew of morning earnings and economic reports followed by an FOMC decision, anything is possible. Traders will have to be in top form to navigate the minefield of news that could create very volatile price action in reaction. Plan carefully, stay focused, and flexible while weighing the considerable risk in such a new driven environment.

Stocks opened down slightly, then ground sideways until 3 pm when a late-day selloff closed us on the lows Tuesday. Overall, it was a blah summer day, seeming to wait on Fed news or some other catalyst. On the day, SPY closed down 0.59%, DIA down 0.76%, and QQQ down 1.27%. Oddly on a down day, VXX also closed down to 29.17, but as expected T2122 also fell just a touch to 78.07. 10-year bond yields were flat at 0.579% and Oil (WTI) fell back to $40.93/barrel. On the upside, Gold closed at another all-time high.

During the afternoon, the Fed announced it is extending its pandemic loan programs (previously planned to end in September) through at least the end of the year. At the same time, Senate Majority Leader McConnell was telling the press what he refuses to negotiate with Democrats and other Republican Senators were saying they oppose the GOP plan. Not to be outdone, Senate Minority Leader Schumer was attacking the Republican plan from the opposite direction.

Last evening, V reported sharply lower revenue and earnings. The company said that even as the country was reopening in June, they saw spending using their cards down 10% during the month (which was actually an estimate beat). BBY also announced that they will join the bandwagon of companies that will not open Thanksgiving Day.

In the US, the virus numbers show we have 4,498,475 confirmed cases and 152,343 deaths. With new cases came in at 64,729 Tuesday and deaths more than doubled day-to-day to 1,245. FL and NC both reported a record number of virus hospitalizations Tuesday. However, FL also reported a bit less than their 7-day average of new cases. Outbreak fears seem to have shifted from the sunbelt to the IN, OH, KY, and TN area.

Globally, the number of cases has reached 16,923,001 confirmed cases and 664,191 deaths. UK PM Johnson warned of a second wave in Europe. This came as the UK and Germany both toughened their travel restrictions for Spain based on an outbreak in the Barcelona region. This came as the Spanish PM warned tougher measures will be needed unless the spread is broken in the next 10 days. In Asia, the Vietnamese PM said every city and province in his country is now at high risk for infection and that they will institute strict lockdowns. Hong Kong Chief Executive Lam said the city was on the verge of a crippling outbreak as well.

Overnight, Asian markets were mixed yet again, with Japan and India significantly lower, but China strongly higher. The rest of the national bourses were mixed and closer to flat. In Europe, a similar scene is taking place with the only significant moves being France to the upside and Italy to the downside so far on Wednesday. In the US, as of 7:30 am futures are pointing to a flat to mildly green open.

The major economic news for Wednesday includes June Trade Balance and June Retail Inventories (both at 8:30 am), June Pending Home Sales (10 am), Crude Oil Inventories (10:30 am), FOMC Statement and Rate Decision (2 pm), and the FOMC Press Conf. (2:30 pm). Major earnings include AAN, AER, ANTM, ADP, AXTA, BA, BSX, BCO, BG, CLS, GIB, CME, ENB, EPB, ETN, ETR, GD, GE, GM, HES, IPG, MGLN, MKL, NSC, OC, PAG, R, SNY, SC, SMG, SPOT, TROW, TEL, and TT all before the open. Then after the close, ADM, AMP, APA, AR, ASGN, AVTR, CCI, CERN, CTSH, CXO, EQIX, FBHS, FTI, LRCX, PYPL, QCOM, QRVO, NOW, SFM, TPC, URI, and YUMC.

With the FOMC not until afternoon and the government arguing over who gets what money and which politician gets the credit, it looks like earnings will drive any move prior to the Fed. And while the FOMC is not expected to make any policy moves, the market is waiting for either reassurance or a scare from Chair Powell’s comments. So, while we will likely see volatility in spots, it would not be unexpected to see drift until 2pm. Also, remember that most Fed moves see a whipsaw 10-15 minutes after the initial move.

Keep an eye on those FAANG stocks as our “canary in the coalmine” and follow the trend. Don’t try to predict reversals, don’t chase moves that got away, and always take profits as you go. Remember, trading is a job and we’re here to consistently make profits, not win the lottery.

Ed

The Daily Swing Trade Ideas for today: NIO, GM, XLU, KR, HOG, YNDX, ZS, IYR, BAC. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The tech giants MSFT, AAPL, GOOG, FB, and AMZN had nice rallies yesterday, lifting the indexes while the vast majority lacked the volume to break choppy consolidation ranges. Please make no mistake that price patterns of stocks and the indexes remain bullish; however, there appears to be a palpable uncertainty as we ramp up earnings. With a busy day of earnings reports, a reading on Consumer Confidence, and the beginning of the 2-day FOMC meeting, anything is possible, and price volatility could be challenging.

Asian markets were mixed but mostly higher overnight with modest gains in the SHANGHAI and HIS. European markets are flat to slightly lower this morning amid stimulus hopes and rising US/China tensions. US Futures are lifting off of morning lows but continue to point to a modestly lower open ahead a big day of earnings and economic data. Remain focused and flexible as anything is possible.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a big day with 93 companies reporting results. Notable reports include MMM, AMD, AFL, AKAM, MO, AMGN, CAR, BXP, CNC, DB, GLW, DHI, DENN, EBAY, ECL, FEYE, BEN, HOG, JBLU, JNPR, MCD, MDLZ, MSCI, OKE, PFE, RTX, ROK, ROP, SPGI, STX, SHW, STAG, SBUX, TRU, V, WH, & YNDX.

News & Technical’s

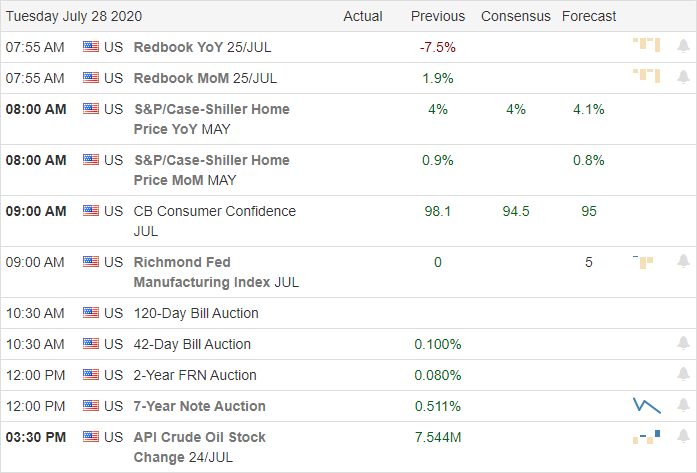

The Senate unveils their version of the coronavirus relief plan with $1200 stimulus checks and $500 for dependents. The bill includes a replacement of 70% of unemployed wages in the extended benefits. There is also considerable funds to help schools trying to get back work this fall. The President’s national security advisor Robert O’Brien has tested positive for COVID, but hot states are starting to show signs of slowing infection rates. However, major league baseball postponed two games yesterday of their shortened season due to several players testing positive. Today begins a marked increase in earnings season ramps up to a fevered pitch with several big tech reports on the way Wednesday and Thursday. Today also starts the 2-day FOMC meeting that culminates in a 2 PM Eastern announcement Wednesday afternoon. According to consensus estimates, the Consumer Confidence numbers expect a small decline when they are released a 10 AM Eastern.

Yesterday saw nice gains in APPL, AMZN, GOOG, FB & MSFT but, the majority of stock found it challenging to find enough volume to move out of choppy consolidation ranges. Futures opened trading last night positive but have since shown some hesitation ahead of busy earnings calendar. Although the VIX pulled back yesterday, it remains quite elevated closing above a 24 handle. So as a few tech giants do the majority of the lifting, there seems to be a palpable uncertainty that the majority of stocks will have some trouble supporting current prices. Only time will tell, but traders should prepare for considerable volatility as we progress through this new laden week. Be careful not to overtrade staying focused on price action flexible as the market reacts to all the data.

A quarter percent higher open led to a roller-coaster morning. However, an afternoon rally saw markets close near their highs, particularly on strength from the mega-cap tech stocks. The QQQ gained 1.78%, SPY gained 0.74%, and DIA gained 0.48%. The VXX closed down to 29.34 and T2122 settled right on the edge of overbought territory at 80.08. 10-year bond yields rose a bit to 0.610% and Oil (WTI) also rose slightly to $41.61/barrel. It’s also worth noting that gold soared to a record high of $1,931.50/oz.

Last evening INTC announced their head of Engineering (who was widely expected to be the next CEO) will leave the company next Monday. No word on if or how this relates to INTC’s announced engineering and manufacturing delays. Unrelated, but about the same time, T subsidiary Warner Brothers also announced that their widely-anticipated new high-budget film Tenet will be released internationally first and then a few weeks later in select US cities in an attempt to reduce virus impact. GOOG announced they are extending their work-from-home plan through at least July 2021. Finally, MCD reported early this am with a 30% revenue drop and a same-store sales short-fall of just 2.3%.

In the US, the virus numbers show we have 4,433,532 confirmed cases and 150,450 deaths. With new cases falling to 61,571 and deaths down to 596, there are signs of plateauing again in at least the 3 worst-hit states (FL, TX, and AZ). Better yet, PFE announced that they had started their phase 3 trial in conjunction with German biotech partner BNTX. This was a timeline acceleration to avoid falling behind MRNA whose own phase 3 trials also began on Monday. It will take a couple of weeks to enroll enough participants in either study and the preliminary results ought to be available as soon as the end of October.

Globally, the number of cases has reached 16,672,852 confirmed cases and 657,270 deaths. The numbers are worrying. However, the real issue of concern is that even the countries that actually acted fast and decisively, and seemingly had the virus under control, are now seeing a resurgence. Among these are China, Hong Kong, Vietnam, Japan, and South Korea. The obvious question is if countries with extremely high mask compliance and fast, strict quarantines have trouble controlling this virus, what does that imply for much less compliant and much more economically-focused countries like the US?

Overnight, Asian markets were mixed again, but leaning more to the green side. China, South Korea, and India all put up gains of over 1%. Japan, Australian, and Thailand were the losers on the day, but not down as much as the winners were up. In Europe, markets are much more on the red side so far in the day. The moves are modest, but the red is broad-based with only Greece, Belgium, and the FTSE on the green side. In the US, as of 7:30 am futures are pointing to a gap lower a third of one percent at the open.

The only major economic news for Tuesday is Conf. Board Consumer Confidence (10 am). However, there are a lot of major earnings with ABG, BEN, CMI, CNC, DHI, DTE, ECL, GLW, HOG, HUN, IVZ, LH, LW, MCD, MDC, MLM, MMM, MO, OMC, PFE, PII, ROP, RTX, SPGI, SHW, XRX, and ZBRA are all among those reporting before the open. After the close, AMD, AFL, AKAM, AMGN, CAR, CB, CHRW, CE, CYH, EBAY, EIX, FTV, THG, JNPR, MDLZ, MRC, NCR, OKE, PKG, SBUX, SSNC, STX, UNM, and V all report.

Monday gave us morning indecision and an afternoon rally (perhaps on Fed hopes). However, nothing really changed in the trend or chart. While it was a decent candle in the QQQ, we still did not print a Morning Star, the bullish trend remains in place, and there remains work ahead if bulls plan to push up through the top again.

Today is a light day on planned news and may well be driven by earnings, hopeful vaccine news, and politicking over stimulus. However, we could also sit on our hands for a day waiting on reassurance from the Fed.

Keep an eye on those FAANG stocks as our “canary in the coalmine.” Follow the trend, don’t chase or predict reversals, and always take profits as you go. Remember, trading is a job and we’re here to consistently make profits, not win the lottery.

Ed

The Daily Swing Trade Ideas for today: WU, XHB, COF, IBM, OIH, HAL, DFS, SLB, HPR, XLV, VXX. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stimulus, huge earnings & economic reports that include an FOMC announcement, pandemic, and rising tensions between the US and China set the stage for a very newsy and potentially volatile market week ahead. Traders could see significant morning gaps, whipsaws, and quick intraday reversal in reaction to all the news coming our way this week. Experienced day traders may have the upper hand this week, while new or inexperienced traders may find it better to stand aside protecting their capital as the market grapples with all the news.

Asian markets closed mixed but mostly lower overnight. European markets trade mixed and primarily flat this morning as US/China tensions and pandemic impacts weigh on investors. US Futures, however, fueled up on another trillion in government stimulus is green across the board and looking for a bullish gap open.

Economic Calendar

Earnings Calendar

We have a hectic week of big earnings reports, but we kick it off this Monday, with 51 companies stepping up with quarterly results.

New and Technical’s

We have an incredibly busy week of news that has the potential to affect the overall market price volatility. We have a big week of earnings reports that include AAPL, MSFT, FB, GOOG & AMZN. An FOMC meeting announcement Wednesday afternoon economic calendar that also includes Durable Goods, Consumer Confidence, GDP, Jobless Claims & Personal income, and Outlays. A likely stimulus bill, topping 1 trillion, that’s an apparent political football gaining headlines and creating turbulence moving its way through congress. Not to mention the growing tensions between the US and China as well as pandemic news that continues to threaten the economy. Traders should prepare for significant morning market gaps, possible whipsaws, intraday reversals, and considerable price volatility as investors grapple with all the reports.

Last week’s pullback left behind some unfavorable price patterns in the index charts that hint of some pricing stress yet, at the same time, maintain bullish overall trends. Some short-term price supports broke while longer-term supports held fast, adding to the complexity of such a newsy week of potentially market-moving news. Traders will have to remain flexible and consider carefully consider the risks of holding any positions overnight due to likely volatility. Plan carefully, and buckle up for what could be a very wild week.

Markets gapped down Friday and then gave us indecision to end the week. Both the SPY and DIA printed Doji and QQQ printed a White Spinning Top. Only the SPY broke its uptrend line, but only the QQQ flipped its Volatility Stop (10. 1.5) from green to red. For the day, the SPY lost 0.64%, the DIA lost 0.75% and the QQQ lost 0.95%. VXX was also flat at 30.17 and T2122 fell back into the mid-range at 66.97. 10-year bond yield were flat at 0.587% and Oil (WTI) climbed slightly to $41.34/barrel. For the week, we had indecisive trading that closed down a bit as once again the mega-cap tech names led markets by the nose all week.

This week has the potential to be the most news-filled of the summer (at least so far). Republicans are expected to finally finish their relief plan so that negotiations can begin with Democrats, perhaps as soon as Monday. Over the week, there will also be 1,200 major earnings reports released, including most of the huge FAANG stocks that truly drive market direction. The CEOs of those FAANG stocks will also be testifying before Congress during an Antitrust hearing on Wednesday. On that day, the Fed also ends its regular meeting and although no new announcements are expected, their statement and the Q/A will be important. Lastly, on Thursday the first read of Q2 GDP will come out, giving us as idea how bad the economy crashed during the first belated shutdown. On top of all this, we know virus and virus impact news will continue hot and heavy.

On Sunday, Bloomberg reported the big banks such as BAC, GS, and JPM now expect the EU’s economic recovery to be larger and faster than that of the US. The overall theme is that leadership and fast action breed public confidence and the EU scores much better at this than the US. Those experts point to July PMI data, where the EU PMIs handily beat analyst expectations, while the US PMI came in below expectations. In the longer-term, the EU will also have much less debt to pay off. The US has spent a bit more than $10 Trillion (so far) in combined fiscal and monetary stimulus (not including state spending). By contrast, the supposedly socialist EU, with a 50% larger population, has spent a fourth of that number even including individual EU-member spending. The bottom line is that companies focused on EU markets may be favored over those that focus on US markets in the short to medium-term timeframes.

In the US, the virus numbers show we have 4,371,992 confirmed cases and 149,852 deaths. Over the weekend, the country saw the 7-day averages rise to 69,000 new cases and 937 new virus deaths. On Friday, MCD and CMG both also joined the long list of retailers now requiring all customers to wear masks. Thankfully, TX and AZ saw a reduction in new reported cases. However, this may be less a trend and more about the hurricane and normal weekend activities impacting numbers.

Globally, the numbers have reached 16,446,932 confirmed cases and 652,852 deaths. It took just over 4 days for the world to go from 15 million to 16 million cases and that pace continues. This came as new outbreaks were found in China, Hong Kong, Vietnam, Japan, Spain, Sweden, Romania, and Bulgaria. The Chinese outbreak was the largest since the initial Wuhan eruption. The W.H.O. also reported rampant spread throughout sub-Saharan Africa. Finally, Latin American has become the current epicenter with Brazil, Mexico, Peru, and Chile now all among the top 8 most-infected countries.

Overnight, Asian markets were mixed but generally close to flat. The exception was Thailand, where in addition to other news items, they are experiencing public demonstrations related to both government response and social problems. (Not a great atmosphere in a country prone to military dictatorships.) In Europe, markets are following Asia. The major bourses are all within a quarter percent on either side of flat so far today. In the US, as of 7:30 am futures are pointing to a gap higher of between a third (DIA) and one percent (QQQ) at the open.

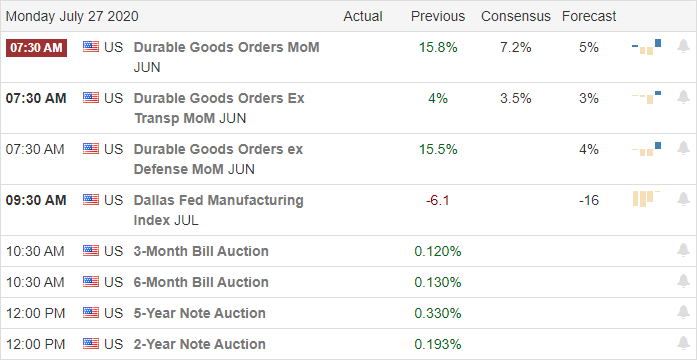

The only major economic news for Monday is June Durable Goods Orders (8:30 am). However, Monday is the slow kickoff of an otherwise heavy week of earnings. Before the bell Monday, we’ll get reports from AVY, CX, EQT, HAS, RPM, and SAP (SAP announced a spinoff IPO of a division as well). After the close, AMKR, BRO, CINF, FIX, CR, EHC, FFIV, NOV, NXPI, OMF, PFG, TFII, and UHS report.

Friday gave us indecisive follow-through to Thursday’s ugly candles, but the uptrend has not been broken and we have potential support below. So, the fight is still on between the bulls and bears in the short-term. We have a lot of news coming this week, which leaves open the possibility of either a lot of volatility or a flat market too overwhelmed by conflicting news to make a move.

That said, remember that the market has only paid attention to good news for months now. The point is we may see a pause to get more assurance, but the lean is definitely still in the bulls favor. So, watch those FAANG stocks as our “canary in the coal mine,” but follow the trend. Don’t chase or predict reversals, and always take profits as you go. Remember, consistent singles and doubles win championships, not occasional home runs.

Ed

The Daily Swing Trade Ideas for today: BBY, LULU, AA, FDX, WEN, KO, TGT, TCOM, DNKG. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Rising joblessness due to growing pandemic pressures and increasing tensions between the US and China had bears asserting themselves yesterday afternoon. Intraday charts indicate a little caution may be in order as we head into the uncertainty of the weekend, but as of now, the daily bullish index trends remain intact. With another big government stimulus plan on the way, it may be difficult for the bears to follow-though on yesterday’s selling. I would not expect the bulls to give up easily as they bask in the glow of newly printed money.

Asian markets saw red across the board during the night as rising US/China tensions weigh on investors. European markets are also in the red this morning after China orders the closing of a US consulate in retaliation. US Futures currently point to modest declines as we wait on new home sales data and earnings. Expect price volatility to remain high as we head into the uncertainty of the weekend.

Economic Calendar

Earnings Calendar

On the Friday, we have 45 companies set to report quarterly results. Notable reports include AXP, BLMN, HON, NEE, NEP, SLB, & VZ.

News and Technical’s

The market had to deal with the prospect that the pandemic is having severe impacts on national joblessness. There are nearly 30 million Americans unemployed far more than the worst of the 2008 financial crisis. The US has now reached another grim record topping 4 million infections, and yesterday, Florida record a record daily death toll. Yesterday, the President suggested that some schools may have to delay reopening and also canceled parts of the upcoming GOP convention. If that were not enough uncertainty for the market to deal with China last night made its retaliatory move in the dangerous game with the US. China has now ordered the US to close the consulate in Chengdu. In a fiery speech, Secretary of State Mike Pompeo’s slammed the Chinese government for its actions while attempting to rally the Chinese people against the Communist Party. According to reports, the Senate expects to unveil its coronavirus relief pan next week, adding yet another wrinkle for the market to grapple with heading into an uncertain weekend.

Although we did see some significant selling yesterday afternoon, the daily technicals of the index charts remain bullish, with the short-term uptrends still intact. The big question for today is, with the mounting economic pressures of the pandemic can the bulls find the energy to defend price supports heading into the weekend. Keep an eye on the tech giants that have led this historic market rally. Should they begin to experience some profit-taking, it may be tough for the indexes to maintain current trends.

Markets gapped down slightly Thursday on worse than expected Initial Jobless Claims (1.4mil vs. 1.3mil expected). However, prices bobbed around flat until Noon, when a strong selloff took us to the lows where prices remained the rest of the day. All 3 major indices put in ugly black candles but did manage to close up off the lows a bit. So, despite the bad day, the bullish trend was not broken. On the day SPY lost 1.19%, DIA lost 1.22%, and QQQ lost 2.61% as the mega-cap tech names led markets lower. The VXX closed up to 30.07 and T2122 fell a bit to 89.47, which is still well into overbought territory. 10-year bond yields fell again as money chased bond safety, closing at 0.577%. Oil (WTI) was also down, closing at $41.06/barrel.

The GOP continues to haggle over their stimulus proposal. Late Thursday Senate Majority Leader McConnell said Senate Republicans will release their plan sometime next week. The Republican plan is expected to be in the $1-1.5 Trillion range and the Democratic plan proposed $3.5 Trillion. So, we’d expect the final number to be in-between the two extremes.

After the close, INTC beat on the top and bottom lines, but guided down for Q3 and announced yet another delay in their next-generation chips (which is already a couple years behind schedule and had been planned for a release 2021). INTC now plan for that 7nm chip release to be in late 2022 or even 2023. (INTC still uses 14nm and competitor AMD has been shipping 7nm chips since 2019.) After-hours, INTC stock was hammered and AMD was up by about the same amount that INTC was down.

In the very suspiciously-timed US-China relations story, the Trump Administration continued to ramp up the “good guy vs. bad guy” theme in yet another scathing speech overnight by Sec. of State Pompeo. Of course, as promised, China retaliated over the US closing the Chinese Houston Consulate by forcing the closure of the US Chengdu consulate. Asian and European markets reacted poorly to these escalations, which traders fear could lead to another trade war.

On the COVID story, in the US, the virus numbers show we have 4,170,333 confirmed cases and 147,342 deaths. The country saw just over 69,100 new cases and 1,150 new virus deaths on Thursday. DIS also announced it is pushing back the release of several major movie franchises for a year over virus fears. These include Mulan, Star Wars, and Avatar. Not coincidentally, AMC theatres also have pushed back their reopening until at least mid-Aug. in light of the current surge in cases nationwide.

Globally, the number of cases has reached 15,684,371 confirmed cases and 637,222 deaths. Brazil had its second-highest number of cases Thursday as the outbreak continues in that country. Cases in that South American country have tripled in the last 30 days. A little further North, China offered Latin American and Caribbean countries a $1 billion low-interest loan to help them finance the purchase of a Covid-19 vaccine. In Asia, both India and Japan again reported their highest number of daily infections on Thursday.

Overnight, Asian markets were down on the US-China tensions. Prices were off significantly across the board, but Shanghai (-3.86%) and Shenzhen (-5.00%) took the hardest hit. In Europe, a similar case is taking shape. All the European bourses are down significantly, with the sole exception of Russia, which is just on the green side of flat so far today. In the US, as of 7:30 am futures are pointing to a modest gap lower of about three-tenths of a percent with the exception of the QQQ which is looking at three-quarters of a percent gap down.

The major economic news for Friday includes July Mfg. PMI and July Services PMI (both at 9:45 am) as well as June New Home Sales (10 am). Major earnings releases include AXP, BLMN, FMX, HON, NEE, SLB, and VZ all before the open.

Thursday’s ugly candles still managed to maintain the uptrend, but we are right there. So, it will be important to see whether the bears can get some follow-through or the bulls can bounce us up off trend and back into the green for the week. Continue to expect volatility as virus news, stimulus rumors, earnings, and the US-China stories are all likely to make headlines today.

As Swing Traders, all we can do is watch the chart and follow the trend. Remember to keep an eye on those FAANG stocks as our “canary in the coalmine.” Remain focused on short-term charts and don’t chase, don’t predict, and always take profits as you go. In earnings season, be wary of both reactions and re-reactions. And don’t forget it’s Friday. So take some profits and be prepared to weather the weekend news cycles.

Ed

The Daily Swing Trade Ideas for today: LABD, XLF, XOP, ITB, XHB, XLE, XLI, XLB, XRT, VXX. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service